合并報表中g(shù)oodwill如何單獨(dú)重點(diǎn)記憶,?

老師您好,,

請問為什么講義上算goodwill的(b)點(diǎn)寫的是identifiable net asset and liabilities? 正常不應(yīng)該是identifiable net asset即equity部分嗎,?

謝謝老師

問題來源:

|

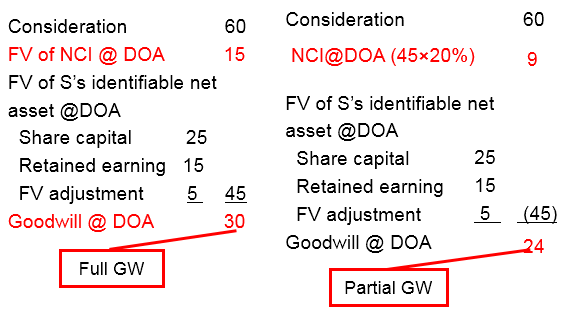

W2 Goodwill |

|

|

|

Consideration |

|

60 |

|

FV of NCI @ DOA |

|

15 |

|

FV of S’s identifiable net asset @DOA |

|

|

|

Share capital |

25 |

|

|

Retained earning |

15 |

|

|

FV adjustment |

5 |

(45) |

|

GW@DOA |

|

(30) |

FV of non-controlling interests:

The non-controlling interests in a subsidiary to be measured at DOA in one of two ways:

(i) At their fair value (i.e. how much it would cost for the acquirer to acquire the remaining shares), or

(ii) At the non-controlling interest's proportionate share of the fair value of the acquiree's identifiable net assets. (only acquirers GW will be calculated)

Note that a parent can choose which method to use on a transaction by transaction basis.

[手寫板]

(60-45×80%)+(15-45×20%)=24+6=30

(60-45×80%)+(45×20%-45×20%)=24+0=24

|

Consideration |

|

60 |

|

FV of NCI @ DOA |

|

15 |

|

FV of S’s identifiable net asset @DOA |

|

|

|

Share capital |

25 |

|

|

Retained earning |

15 |

|

|

FV adjustment |

5 |

(45) |

|

Goodwill at DOA |

|

(30) |

FV of the identifiable assets and liability

The general rule is that, on acquisition, the subsidiary's assets and liabilities must be recognised and measured at their acquisition date fair value.

特別關(guān)注:

1. intangible assets

Recognised separately from goodwill only if they are identifiable. It is identifiable only if it:

(a) is separable, ie capable of being separated from the entity and sold or exchanged. (能夠從被投資方分離)

(b) arises from contractual or other legal rights(源于合同性權(quán)利或法定權(quán)利)

例: research expenditure, brand name, domain name, customer list

2. Contingent liability

Contingent liability of the acquiree are recognised if their fair value can be measured reliably. A contingent liability must be recognised even if the outflow is not probable, provided there is a present obligation.

3. expected future loss

Liability for future loss should NOT be recognised, because it is not a present obligation.

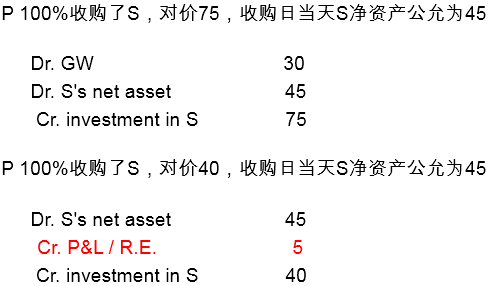

Goodwill:

GW should be recognised on a business combination. This is calculated as the difference between:

(a)The aggregate of the fair value of the consideration transferred and the non-controlling interest in the acquiree at the acquisition date, and

(b)The fair value of the acquiree’s identifiable net assets and liabilities

Negative Goodwill - Bargain purchase

Before recognising a gain on a bargain purchase, the acquirer shall reassess (review):

(i) whether it has correctly identified all of the assets acquired and all liabilities assumed

(ii) whether the fair value of the assets acquired and all liabilities assumed are correctly determined

(iii) measurement of consideration

Acquirer shall recognise the resulting gain in profit or loss (increasing R.E.) on the acquisition date. The gain shall be attributed to the acquirer.

Measurement period

During the measurement period, the acquirer shall retrospectively adjust the provisional amounts recognised at the acquisition date to reflect new information obtained about facts and circumstances that existed at the acquisition date and, if known, would have affected the measurement of the amounts recognised at that date. The measurement period shall not exceed one year from the acquisition date. (12月原則)

遲老師

2021-08-29 03:29:57 1495人瀏覽

在合并報表中g(shù)oodwill要單獨(dú)重點(diǎn)記憶,這里的B 說的是母公司為了收購子公司付出的公允價值,題目中可能會涉及現(xiàn)金形式收購,,以股票形式收購,以債劵形式收購等問題

每個努力學(xué)習(xí)的小天使都會有收獲的,,加油,!相關(guān)答疑

-

2022-08-30

-

2022-07-10

-

2021-08-21

-

2021-05-30

-

2021-04-23

您可能感興趣的ACCA試題

- 單選題 IMA管理會計(jì)聲明中“價值觀和道德觀:從接受到實(shí)踐”表明持續(xù)的培訓(xùn)應(yīng)包括下列所有內(nèi)容,除了( ),。

- 單選題 某投資者一年前以每股40美元的價格購得股票,每年的股息為1.50美元,。目前該股的價格為45美元,,持有該股票一年的收益率是多少( ),。

- 單選題 投資者已經(jīng)收集了以下四種股票的信息: 股票 β 平均收益(%) 回報的標(biāo)準(zhǔn)差(%) W 1.0 9.5 13.2 X 1.2 14.0 20.0 Y 0.9 8.4 14.5 Z 0.8 6.0 12.0 風(fēng)險最低的股票是( ),。

津公網(wǎng)安備12010202000755號

津公網(wǎng)安備12010202000755號