英語不好見諒,,I.P和O.P分別是什么意思,?

op,ip 具體英語? 能不能給一些縮寫的翻譯+具體英文,,這樣好理解一點(diǎn),。否則看的太累了。

問題來源:

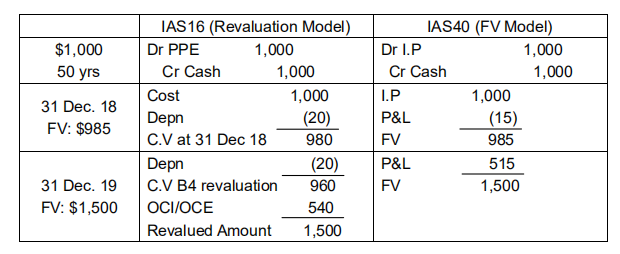

2.4 Measurement after recognition

2.4.1 Fair value model

Any change in fair value reported in profit or loss, not depreciated. Under the fair value model, the entity remeasures its investment properties to fair value each year. No depreciation is charged. All gains and losses on revaluation are reported in the statement of profit or loss.

(不折舊,,年年估,進(jìn)損益)

2.4.2 Cost model

As cost model of IAS16.

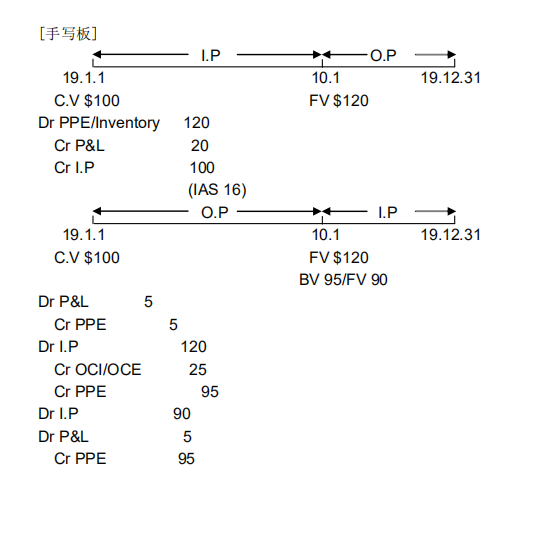

2.5 Transfers to or from investment properly

Transfers to or from investment property should only be made when there is a change in use (IFRS 40: para. 57). A change in management's intentions for the use of a properly does not provide evidence of a change in use (IAS 40: para. 57).

2.5.1 Transfer from I.P. to O.P. or inventories

Use the fair value at the date of the change for subsequent accounting under IAS16 or IAS2. (公允口徑入賬,,公允與賬面差額入當(dāng)期損益)

2.5.2 Transfer from O.P. to I.P.

Normal accounting under IAS 16 (cost less depreciation) will have been applied up to the date of the change. On adopting fair value, any increase is recognised as other comprehensive income and credited to the revaluation surplus in equity in accordance with IAS 16. If the fair valuation causes a decrease in value, then it should be charged to profits. (公允口徑入賬, 公允>賬面 OCI/公允<賬面 P&L)

2.5.3 Transfer from inventory to I.P.

Any change in the carrying amount caused by the transfer should be recognised in P&L. (公允口徑入賬, 公允與賬面差額入當(dāng)期損益)

王老師

2021-12-12 20:06:24 1863人瀏覽

I.P即Investment property,中文為投資性房地產(chǎn),。

O.P即Owner-occupied property,,中文為自用房地產(chǎn)。

每個(gè)努力學(xué)習(xí)的小天使都會有收獲的,,加油,!相關(guān)答疑

-

2025-06-26

-

2025-06-14

-

2022-08-30

-

2022-07-10

-

2022-07-05

您可能感興趣的ACCA試題

- 單選題 某投資者一年前以每股40美元的價(jià)格購得股票,,每年的股息為1.50美元。目前該股的價(jià)格為45美元,,持有該股票一年的收益率是多少( ),。

- 單選題 投資者已經(jīng)收集了以下四種股票的信息: 股票 β 平均收益(%) 回報(bào)的標(biāo)準(zhǔn)差(%) W 1.0 9.5 13.2 X 1.2 14.0 20.0 Y 0.9 8.4 14.5 Z 0.8 6.0 12.0 風(fēng)險(xiǎn)最低的股票是( )。

- 單選題 公司賣出了一個(gè)看跌期權(quán),,行權(quán)價(jià)格為$56,同時(shí)購買了一個(gè)行權(quán)價(jià)格為$44的看漲期權(quán),;購買期權(quán)時(shí)股票的價(jià)格為$44,;看漲期權(quán)費(fèi)為$5,看跌期權(quán)費(fèi)為$4,目前的價(jià)格上漲了$7,,那么ABC公司因?yàn)榭礉q期權(quán)取得或是損失的金額為多少( ),。

津公網(wǎng)安備12010202000755號

津公網(wǎng)安備12010202000755號