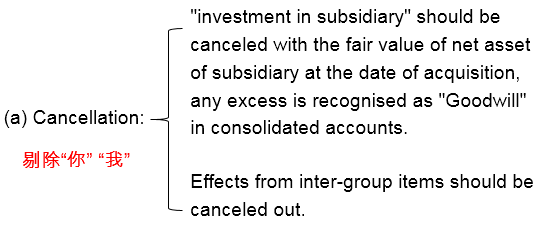

Business combination

老師您好,

(1)我想請問 IFRS3 Business combination和 IFRS10 Consolidated financial statement所包含的內(nèi)容有什么區(qū)別,?

(2)在企業(yè)合并時,,子公司有一項或有負(fù)債,,在合并后要確認(rèn)這項或有負(fù)債嗎,?

謝謝老師

問題來源:

Study Guide:

1. Subsidiary

2. Associate

3. Comprehensive example

1. Subsidiary

General steps of consolidation:

(b) Adding up all uncanceled assets and liabilities on a line by line basis, by doing (a)and (b), we are consolidating as if parent owned everything in subsidiary

體現(xiàn)100%的控制

(c) show the extend to which you do not own

|

說實話 |

合并B/S |

|

合并I/S |

引入案例:

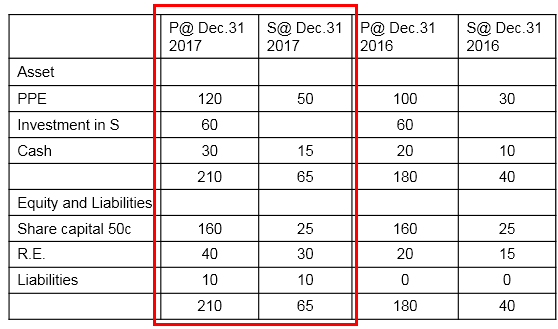

P acquired 80% of S on 31 Dec. 2016 for $60. FV of a building in S is $5 higher than its NBV, which has remaining useful life of 5 years. FV of NCI at DOA is $15.

@ DOA in P's a/c

Dr. Investment in subsidiary 60

Cr. Cash 60

A parent company will usually produce its own single company financial statements and these should be prepared in accordance with IAS 27(revised) Separate financial statements. In these statements, investments in subsidiaries and associates included in the financial statements should be either:

(a) Accounted for at cost, or

(b) In accordance with IFRS 9

(c) equity method

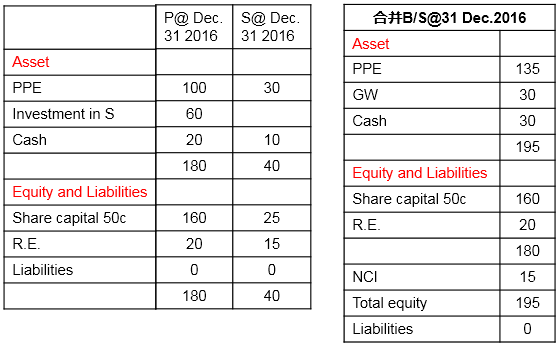

W2 Goodwill

|

Consideration |

|

60 |

|

FV of NCI @ DOA |

|

15 |

|

FV of S’s identifiable net asset @DOA |

|

|

|

Share capital |

25 |

|

|

Retained earning |

15 |

|

|

FV adjustment |

5 |

(45) |

|

GW @ DOA |

|

(30) |

我們首先假設(shè)P 100%收購了S

Consideration

FV of S’s identifiable net asset @DOA

Share capital

Retained earning

FV adjustment

|

W2 Goodwill |

|

|

Consideration |

60 |

|

FV of NCI @ DOA |

15 |

|

FV of S’s identifiable net asset @DOA |

|

|

|

Share capital |

25 |

|

|

Retained earning |

15 |

|

|

FV adjustment |

5 |

(45) |

|

Goodwill at DOA |

|

30 |

王老師

2021-08-21 10:15:11 1446人瀏覽

哈嘍,!努力學(xué)習(xí)的小天使:

1.IFRS3企業(yè)合并,,對其他企業(yè)開始控制了,取得控制權(quán)后編制合并報表,, 包含主要的編制原則,。

IFRS10合并財務(wù)報表,企業(yè)成為合并關(guān)系了,,在各期需要編制合并報表時,,根據(jù)開始企業(yè)合并時編制的合并報表的基礎(chǔ)上,根據(jù)期間內(nèi)發(fā)生的業(yè)務(wù)對合并財務(wù)報表各個會計科目進(jìn)行如何處理以及調(diào)整,。

2.在企業(yè)合并時,,或有負(fù)債需要根據(jù)具體情況考慮是否 確認(rèn)為預(yù)計負(fù)債 。

每個努力學(xué)習(xí)的小天使都會有收獲的,,加油,!

相關(guān)答疑

-

2022-08-30

-

2022-07-10

-

2021-08-29

-

2021-05-30

-

2021-04-23

您可能感興趣的ACCA試題

- 單選題 投資者已經(jīng)收集了以下四種股票的信息: 股票 β 平均收益(%) 回報的標(biāo)準(zhǔn)差(%) W 1.0 9.5 13.2 X 1.2 14.0 20.0 Y 0.9 8.4 14.5 Z 0.8 6.0 12.0 風(fēng)險最低的股票是( )。

- 單選題 公司賣出了一個看跌期權(quán),,行權(quán)價格為$56,同時購買了一個行權(quán)價格為$44的看漲期權(quán),;購買期權(quán)時股票的價格為$44,;看漲期權(quán)費(fèi)為$5,看跌期權(quán)費(fèi)為$4,目前的價格上漲了$7,,那么ABC公司因為看漲期權(quán)取得或是損失的金額為多少( ),。

- 單選題 在理性的市場情況下,,下列哪個投資有可能獲得最低的回報率( )。

津公網(wǎng)安備12010202000755號

津公網(wǎng)安備12010202000755號