不是NCI change的子公司處置走什么?

請問處置子公司時:從子公司賣成關聯(lián)方了,,得出來的gain or lose走什么,?

我知道NCI change走OCI

問題來源:

2.Disposal

(a) Full disposal

(b) Subsidiary to investment

(c) Subsidiary to associate

(d) Associate to investment

(e) Subsidiary to subsidiary

2.1Full disposal

Statement of profit or loss and other comprehensive income

Consolidate the results and NCI to the date of disposal.

Show a group profit or loss on disposal.

Statement of financial position

No consolidation (and no non-controlling interests) as there is no subsidiary at the year end

@Date of disposal (計算合并報表角度處置子公司損益)

|

Consideration received |

|

50 |

|

Less: |

|

|

|

CV of S's net asset @DOD(excluding GW) |

60 |

|

|

GW |

2.8 |

|

|

less: NCI% of S's net asset(60×20%) |

(12) |

50.8 |

|

Loss on disposal |

|

0.8 |

2.2 Subsidiary to associate

Partial disposal大體原則:

“Sold” a subsidiary/associate, and therefore derecognise the subsidiary (associate) which will give a group profit or loss on disposal.

“Purchase” an associate/investment which means the retained investment should be remeasured to fair value at the date of disposal.

2.2 Subsidiary to associate

Statement of profit or loss and other comprehensive income

?Treat as a subsidiary to the date of disposal; ie consolidate for correct number of months and show non-controlling interests for that period.

?Show a group profit or loss on disposal.

?Treat as an associate thereafter (ie equity account).

Statement of financial position

?Remeasure the investment retained to fair value at the date of disposal.

?Equity account (FV at date of control lost = cost of associate) thereafter.

2.3 Subsidiary to investment

Statement of profit or loss and other comprehensive income

?Consolidate as a subsidiary to the date of disposal.

?Show a group profit or loss on disposal.

?Show fair value changes (and any dividend income) thereafter.

Statement of financial position

?Remeasure the investment retained to fair value at the date of disposal.

?Investment in equity instruments (IFRS 9) thereafter.

2.4 Associate to investment

Statement of profit or loss and other comprehensive income

?Equity account as an associate to date of disposal.

?Show a group profit or loss on disposal.

?Show fair value changes (and any dividend income) thereafter.

Statement of financial position

?Remeasure the investment remaining to fair value at the date of disposal.

?Investment in equity instruments (IFRS 9) thereafter.

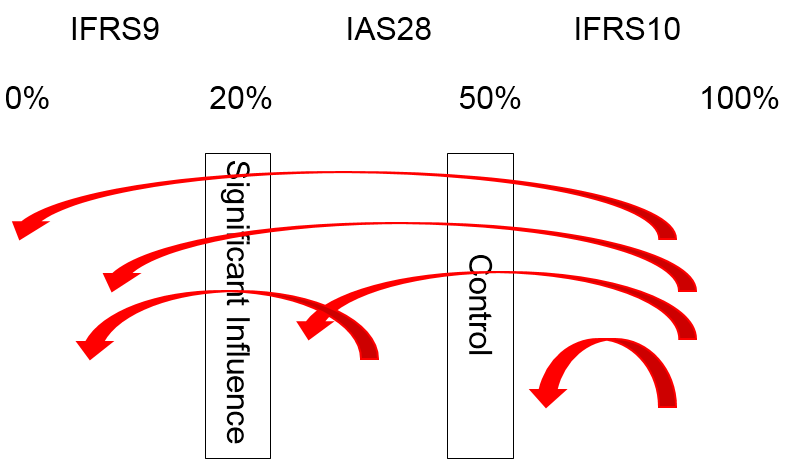

2.5 Sale of shares when control is retained (NCI change)

In group accounts, a sale of shares which results in the parent retaining control is simply a transaction between shareholders. If the parent company holds 65% of the shares of a subsidiary but then sells a 5% holding, a relationship of control still exists. As such, the subsidiary will still be consolidated in the group financial statements. However, the NCI has risen from 35% to 40%

The accounting treatment of the above situation is as follow:

? The NCI within equity is increased

? The difference between the proceeds received and the increase in the non-controlling interest is accounted within equity.

? No profit or loss should be recognised and goodwill should not be recalculated.

3. SUMMARISED STATEMENTS OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME FOR THE YEAR ENDED 30 APRIL 20X4

|

Mart $m |

Pipe $m |

|

|

Revenue |

800 |

230 |

|

COS and expenses |

(680) |

(170) |

|

Profit before tax |

120 |

60 |

|

Income tax |

(30) |

(20) |

|

Profit for the year |

90 |

40 |

|

Other comprehensive income |

||

|

Gain on revaluation |

5 |

10 |

|

T.C.I. |

95 |

50 |

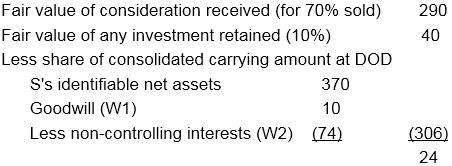

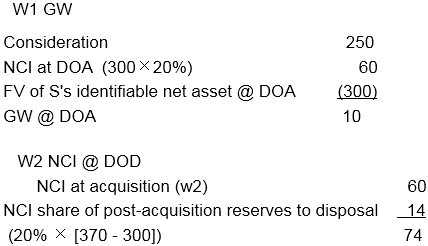

On 1 May 20X2, Mart acquired 80% of the equity interests of Pipe. The purchase consideration comprised cash of $250 million and the fair value of the identifiable net assets acquired was $300 million at that date. Mart wishes to use the partial goodwill method for all acquisitions. There has been no impairment of goodwill in Pipe since acquisition.

Mart disposed of a 70% equity interest in Pipe on 31 October 20X3 for $290 million. At that date Pipe's identifiable net assets were $370 million. The remaining equity interest of Pipe held by Mart was fair valued at $40 million

Required: calculate the group profit on disposal of the shares in Pipe.

文字答案提示:

The finance director has calculated the group profit on disposal incorrectly. Prior to the disposal, X was a 80% subsidiary. After selling a 70% stake, Y is left with a 10% simple investment in X with no significant influence or control. In substance, Y has “sold” a 80% subsidiary and, on the same date, “purchased” a 10% investment. Thus, X should be deconsolidated and a group profit or loss on disposal recognised. The remaining interest should be remeasured to its fair value at the date control was lost.

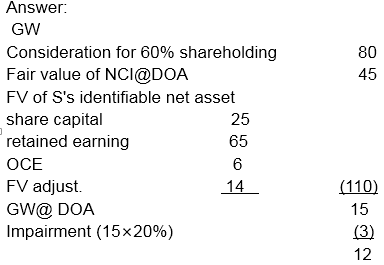

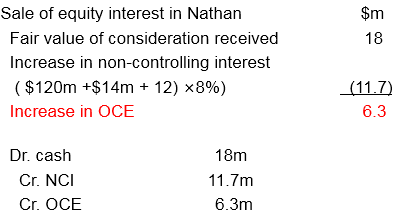

4. On 1 May 2012, Marchant acquired 60% of the equity interests of Nathan, a public limited company. The purchase consideration comprised cash of $80 million and the fair value of the identifiable net assets acquired was $110 million at that date. The fair value of the non-controlling interest (NCI) in Nathan was $45 million on 1 May 2012. Marchant wishes to use the ‘full goodwill’ method for all acquisitions. The share capital and retained earnings of Nathan were $25 million and $65 million respectively and other components of equity were $6 million at the date of acquisition. The excess of the fair value of the identifiable net assets at acquisition is due to non-depreciable land.

Goodwill has been impairment tested annually and as at 30 April 2013 had reduced in value by 20%.

Marchant disposed of an 8% equity interest in Nathan on 30 April 2014 for a cash consideration of $18m. The carrying value of the net asset of Nathan at 30 April 2014 was $120m before any adjustments on consolidation.

遲老師

2021-08-28 13:43:43 1125人瀏覽

得出來的gain與loss應記在資產負債表中的return earning上

每個努力學習的小天使都會有收獲的,加油!相關答疑

-

2025-06-26

-

2025-06-14

-

2022-08-30

-

2022-07-10

-

2022-07-05

您可能感興趣的ACCA試題

- 單選題 某投資者一年前以每股40美元的價格購得股票,每年的股息為1.50美元,。目前該股的價格為45美元,,持有該股票一年的收益率是多少( )。

- 單選題 投資者已經收集了以下四種股票的信息: 股票 β 平均收益(%) 回報的標準差(%) W 1.0 9.5 13.2 X 1.2 14.0 20.0 Y 0.9 8.4 14.5 Z 0.8 6.0 12.0 風險最低的股票是( ),。

- 單選題 公司賣出了一個看跌期權,,行權價格為$56,,同時購買了一個行權價格為$44的看漲期權;購買期權時股票的價格為$44,;看漲期權費為$5,看跌期權費為$4,,目前的價格上漲了$7,那么ABC公司因為看漲期權取得或是損失的金額為多少( ),。

津公網安備12010202000755號

津公網安備12010202000755號