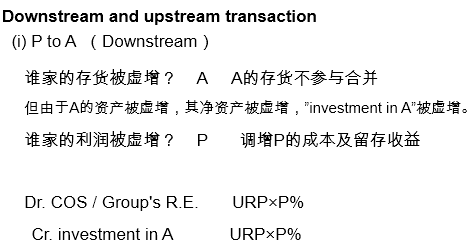

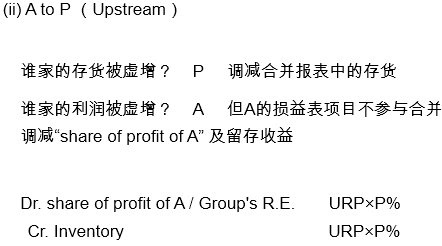

子公司RE計(jì)算為何不計(jì)減值?

請(qǐng)問計(jì)算母公司最后的RE時(shí)要按照持股比例分?jǐn)侴W,,為什么計(jì)算子公司的RE時(shí)不按比例分?jǐn)侴W,?

問題來源:

|

Statement of Financial Position at 31Dec. 20x9 |

|||

|

Bailey $m |

Hill $m |

Camp $m |

|

|

Non-current asset |

|||

|

PPE |

2,300 |

1,900 |

700 |

|

Invest. in Hill |

720 |

||

|

Invest. in Camp |

225 |

||

|

Current asset |

3,115 |

1,790 |

1,050 |

|

Total Asset |

6,360 |

3,690 |

1,750 |

|

Equity |

|||

|

share capital $1 |

1,000 |

500 |

240 |

|

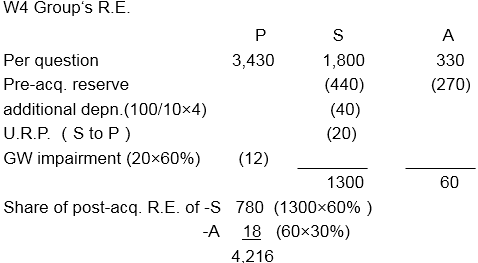

R.E. |

3,430 |

1,800 |

330 |

|

Total equity |

4,430 |

2,300 |

570 |

|

Non-current Liability |

350 |

290 |

220 |

|

Current Liability |

1,580 |

1,100 |

960 |

|

Total E&L |

6,360 |

3,690 |

1,750 |

|

Dividend paid in the year(from post-acquisition profits) |

250 |

50 |

20 |

Bailey, a public limited company, has acquired shares in two companies. The details of the acquisitions are as follows:

|

Coy. |

DOA |

share capital $1 |

RE @ DOA |

FV of net asset at DOA |

Cost of invent. |

share capital acquired |

|

$m |

$m |

$m |

$m |

|||

|

Hill |

1 Jan.2006 |

500 |

440 |

1,040 |

720 |

300 |

|

Camp |

1 May 2009 |

240 |

270 |

510 |

225 |

72 |

|

Statement of Profit or Loss and OCI for the year ended 31Dec. 20x9 |

|||

|

Bailey $m |

Hill $m |

Camp $m |

|

|

Revenue |

5,000 |

4,200 |

2,000 |

|

COS |

(4,100) |

(3,500) |

(1,800) |

|

Gross profit |

900 |

700 |

200 |

|

expenses |

(320) |

(175) |

(40) |

|

Dividend from H & C |

36 |

||

|

Profit before tax |

616 |

525 |

160 |

|

Income tax |

(240) |

(170) |

(50) |

|

Profit for the year |

376 |

355 |

110 |

|

Other comprehensive income |

|||

|

Gain on revaluation |

50 |

20 |

10 |

|

T.C.I. |

426 |

375 |

120 |

|

Consolidated Profit or loss and Other Comprehensive Income |

|

|

Revenue (5000+4200-200) |

9,000 |

|

Cost of sales (4100+3500+10-200+20) |

(7,430) |

|

Gross profit |

1,570 |

|

Distribution and Admin.(320+175+15) |

(510) |

|

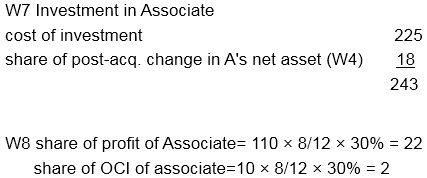

Share of profit of associate (W8) |

22 |

|

Profit before tax |

1,082 |

|

Income tax(240+170) |

(410) |

|

Profit for the year |

672 |

|

Other comprehensive income |

|

|

gain on revaluation(50+20) |

70 |

|

share of gain on revaluation of A (W8) |

2 |

|

Total comprehensive income |

744 |

|

Profit attributable to: |

|

|

Owner of the parent(β) |

548 |

|

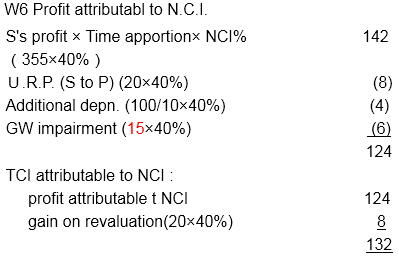

N.C.I. (W6) |

124 |

|

672 |

|

|

T.C.I. attributable to: |

|

|

Owner of the parent (β) |

612 |

|

N.C.I. (W6) |

132 |

|

744 |

|

|

Consolidated Statement of Financial Position |

||

|

Asset |

||

|

N.C.A. |

||

|

PPE |

2300+1900+100-40 |

4,260 |

|

GW (w2) |

110 |

|

|

Invest. in Associate(w7) |

243 |

|

|

4,613 |

||

|

Current asset |

3115+1790-20 |

4,885 |

|

Total asset |

9,498 |

|

|

Equity and liability |

||

|

Share capital |

1,000 |

|

|

Reserves(w4) |

4,216 |

|

|

5,216 |

||

|

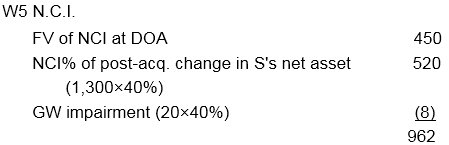

N.C.I. (W5) |

962 |

|

|

Total equity |

6,178 |

|

|

N.C.L. |

350+290 |

640 |

|

C.L. |

1,580+1100 |

2,680 |

|

Total equity and liability |

9,498 |

|

補(bǔ)充:

王老師

2021-04-13 13:35:54 941人瀏覽

在計(jì)算母公司的RE時(shí)是站在合并報(bào)表角度按照對(duì)s 公司的持股比例分?jǐn)侴W,,在計(jì)算S公司RE時(shí)S公司做為一個(gè)整體計(jì)算RE,,無需分?jǐn)偂?br/>

每個(gè)努力學(xué)習(xí)的小天使都會(huì)有收獲的,,加油!相關(guān)答疑

-

2025-06-26

-

2022-08-30

-

2022-07-10

-

2022-07-05

-

2021-08-11

您可能感興趣的ACCA試題

- 單選題 某投資者一年前以每股40美元的價(jià)格購(gòu)得股票,每年的股息為1.50美元,。目前該股的價(jià)格為45美元,,持有該股票一年的收益率是多少( )。

- 單選題 投資者已經(jīng)收集了以下四種股票的信息: 股票 β 平均收益(%) 回報(bào)的標(biāo)準(zhǔn)差(%) W 1.0 9.5 13.2 X 1.2 14.0 20.0 Y 0.9 8.4 14.5 Z 0.8 6.0 12.0 風(fēng)險(xiǎn)最低的股票是( ),。

- 單選題 公司賣出了一個(gè)看跌期權(quán),行權(quán)價(jià)格為$56,,同時(shí)購(gòu)買了一個(gè)行權(quán)價(jià)格為$44的看漲期權(quán),;購(gòu)買期權(quán)時(shí)股票的價(jià)格為$44;看漲期權(quán)費(fèi)為$5,看跌期權(quán)費(fèi)為$4,,目前的價(jià)格上漲了$7,,那么ABC公司因?yàn)榭礉q期權(quán)取得或是損失的金額為多少( )。

津公網(wǎng)安備12010202000755號(hào)

津公網(wǎng)安備12010202000755號(hào)