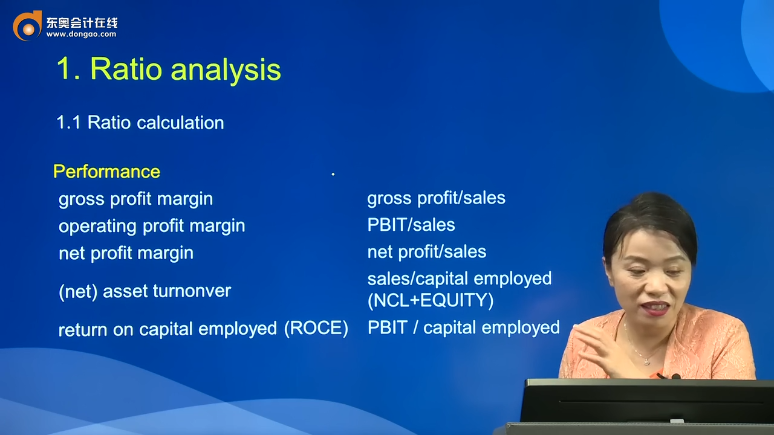

ration caluculation

老師您好,,

請問最后兩個ratio中的capital employed是什么呢,,什么意思,?

謝謝老師

問題來源:

2. Non-financial Reporting

Non-financial reporting enables entities to be more transparent in communicating non-financial elements of their business to their stakeholders. Non-financial reporting can have significant benefits to an entity in terms of its reputation and positive stakeholder engagement.

2.1Environmental reporting

The aim of environmental reporting is the disclosure of an organisation's corporate environmental responsibilities and the effects of its activities on its environment.

2.2 Social report

The aim of social reporting is to measure and disclose the social impact of a business's activities.

Examples of social measures include:

? Philanthropic donations(慈善捐贈)

? Employee satisfaction levels and remuneration issues;

? Community support; and

? Stakeholder consultation information

2.3 Management commentary(管理層評述)

Management commentary: a narrative report that relates to financial statements that have been prepared in accordance with IFRSs. Management commentary provides users with historical explanations of the amounts presented in the financial statements, specifically the entity's financial position, financial performance and cash flows. It also provides commentary on an entity's prospects and other information not presented in the financial statements. Management commentary also serves as a basis for understanding management's objectives and its strategies for achieving those objectives.

The IFRS Practice Statement is a non-binding guidance document rather than an IFRS

It is designed for publicly traded entities, but it is left to regulators to decide which entities are required to publish management commentary and how frequently they should report. This approach avoids the adoption hurdle, i.e. that the perceived cost of applying IFRSs increases, which could otherwise dissuade countries not having adopted IFRSs from requiring its adoption, especially where requirements differ significantly from existing national requirements.

|

Advantages |

Disadvantage |

|

Entity: ?promotes the entity, and attracts investors, lenders, customers and suppliers ?Communicates management plans and outlook |

Entity: ? Costs may outweight benefits ?Risk that investors may ignore the financial statements |

|

Users: ?F.S. not enough to make decision ?F.S. backward looking ?Highlights risks ?useful for comparability |

Users: ?Subjective ?Not normally audited ?Could encourage companies to de-list (avoid requirement to produce MC) |

王老師

2021-08-20 06:28:30 1094人瀏覽

capital employed是指占用的資產(chǎn),。

sales/capital employed是指1元的資產(chǎn)支持多少銷售,,

PBIT/capital employed是指1元的資產(chǎn)帶來多少稅前利潤。

相關(guān)答疑

-

2024-10-27

-

2024-01-09

-

2022-08-30

-

2022-07-10

-

2022-07-05

您可能感興趣的ACCA試題

- 單選題 投資者已經(jīng)收集了以下四種股票的信息: 股票 β 平均收益(%) 回報(bào)的標(biāo)準(zhǔn)差(%) W 1.0 9.5 13.2 X 1.2 14.0 20.0 Y 0.9 8.4 14.5 Z 0.8 6.0 12.0 風(fēng)險(xiǎn)最低的股票是( ),。

- 單選題 公司賣出了一個看跌期權(quán),行權(quán)價(jià)格為$56,,同時(shí)購買了一個行權(quán)價(jià)格為$44的看漲期權(quán),;購買期權(quán)時(shí)股票的價(jià)格為$44;看漲期權(quán)費(fèi)為$5,看跌期權(quán)費(fèi)為$4,,目前的價(jià)格上漲了$7,,那么ABC公司因?yàn)榭礉q期權(quán)取得或是損失的金額為多少( )。

- 單選題 在理性的市場情況下,下列哪個投資有可能獲得最低的回報(bào)率( ),。

津公網(wǎng)安備12010202000755號

津公網(wǎng)安備12010202000755號