W12:NCI最后的計算怎么求,?

請問,這里將172.4的NCI除以40%,還原的意思是什么,? 我理解172.4已經(jīng)是全部NCI的價值了

問題來源:

Study Guide

1.Step acquisition

2.Disposal

1. Step acquisition

(a) Investment to associate

(b) Investment to subsidiary

(c) Associate to subsidiary

(d) Subsidiary to subsidiary

1.1 investment to associate

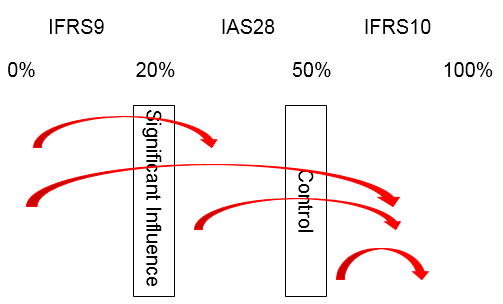

Where an investment in equity instruments becomes an associate, the investment (measured either at cost or at fair value) is treated as part of the cost of the associate.

Statement of profit or loss and other comprehensive income

? Equity account as an associate from the date of significant influence

? Remeasure the investment to FV at the date significant influence achieved

Statement of financial position

? Equity account as associate

1.2 Investment to subsidiary

Statement of profit or loss and other comprehensive income

? Remeasure the investment to FV at the date the parent achieves control

? Consolidate as a subsidiary from the date the parent achieves control

Statement of financial position

? Calculate goodwill at the date the parent achieves control

? Consolidate as a subsidiary at the year end

1.3 Associate to subsidiary

Statement of profit or loss and other comprehensive income

? Equity account as an associate to the date the parent achieves control

? Remeasure the associate to FV at the date the parent obtains control

? Consolidate as a subsidiary from the date the parent obtains control

Statement of financial position

? Calculate goodwill at the date the parent obtains control

? Consolidate as a subsidiary at the year end

1.4 Step acquisition where control is retained (NCI change)

In substance, there has been no acquisition since the entity is still a subsidiary. Instead this is a transaction between group shareholders (ie the parent is buying 10% from the NCI ) and should be acounted for as equity transaction (權(quán)益性交易). Therefore, it is recorded in equity as follows:

(a)Decrease non-controlling interests (NCI) in the consolidated SOFP

(b) Recognise the difference between the consideration paid and the decrease in NCI as an adjustment to equity (post to the parent's column in the consolidated OCE/retained earnings working)

No profit or loss arises on the purchase of the additional shares and goodwill is not recalculated.

1.Alpha acquired a 15% investment in Beta in 1 January 20X6 for $360,000 when Beta's retained earnings were $100,000. At that date, Alpha had neither significant influence nor control of Beta. The fair value of the investment at 31 December 20X8 was $480,000 and at 1 July 20X9 was $500,000.

On 1 July 20X9, Alpha acquired an additional 65% of the 2 million $1 equity shares in Beta for $2,210,000. The retained earnings of Beta at that date were $1,100,000. Beta has no other reserves. Alpha elected to measure non-controlling interest at fair value at the date of acquisition. The non-controlling interest had a fair value of $680,000 at 1 July 20X9. There has been no impairment in the goodwill of Beta to date.

Required

(a) Explain how the investment in Beta would be accounted for in Alpha's group accounts for the year ended 31 December 20X9.

(b) Calculate the gain or loss on remeasurement of the 15% investment at 1 July 20X9 (on the assumption that the investment was still carried at its 31 December 20X8 fair value at that date).

(c) Calculate the goodwill in Beta for inclusion in the consolidated statement of financial position of the Alpha group as at 31 December 20X9.

Answer:

(a)Consolidated statement of profit or loss and OCI

On acquisition of an additional 65% in Beta on 1 July 20X9, Alpha's total shareholding amounted to 80% (15% + 65%), giving Alpha control of Beta. In the consolidated statement of profit or loss and other comprehensive income, Alpha should consolidate Beta for the 6 months that Beta was a subsidiary, pro-rating Beta's income and expenses accordingly (assuming profits accrue evenly).

Since, in substance, Alpha has sold a 15% investment, the investment should be remeasured to fair value on 1 July 20X9 and a gain or loss should be recognised either in profit or loss (if the investment had been measured at fair value through profit or loss) or other comprehensive income (if the election had been made to hold the investment at fair value through other comprehensive income).

Consolidated statement of financial position

In substance, on 1 July 20X9, Alpha purchased an 80% subsidiary. Therefore, goodwill should be calculated on the full 80% shareholding, and, in the consolidated statement of financial position, Beta should be consolidated as a subsidiary.

(b) Gain or loss on remeasurement

|

Fair value at date control achieved (1.7.X9) |

500 |

|

Carrying amount of investment (fair value at previous year end: 31. 12. X8 |

(480) |

|

|

20 |

(c) Calculation of GW

|

Consideration for 65% shareholding |

|

2,210 |

|

Fair value of pre-existing interest |

|

500 |

|

NCI at DOA |

|

680 |

|

FV of S's identifiable net asset |

2,000 |

|

|

share capital |

1,100 |

(3,100) |

|

retained earning |

|

290 |

|

in P's a/c |

(1) Dr. FA |

20 |

|

|

Cr. P&l / OCI |

20 |

|

|

(2) Dr. intestment in S (2210+500) |

2710 |

|

|

Cr. FA |

500 |

|

|

Cr. cash |

2210 |

|

in Group's a/c |

Dr.S's net asset at DOA |

3100 |

|

|

Dr. GW |

290 |

|

|

Cr. N.C.I |

680 |

|

|

Cr. Investment in S |

2710 |

2. Dec. 2009 Q1

On 1 June 20X8, Grange acquired 60% of the equity interests of Park, a public limited company. The purchase consideration comprised cash of $250 million. Excluding the franchise referred to below, the fair value of the identifiable net assets was $360 million. The excess of the fair value of the net assets is due to an increase in the value of non-depreciable land.

Park held a franchise right, which at 1 June 20X8 had a fair value of $10 million. This had not been recognised in the financial statements of Park. The franchise agreement had a remaining term of five years to run at that date and is not renewable. Park still holds this franchise at the year-end.

Grange wishes to use the 'full goodwill' method for all acquisitions. The fair value of the non-controlling interest in Park was $150 million on 1 June 20X8. The share capital was $230m, retained earnings of Park were $115 million and other components of equity were $10 million at the date of acquisition.

Grange acquired a further 20% interest from the non-controlling interests in Park on 30 November 20X9 for a cash consideration of $90 million.

Answer:

|

W3 GW |

|

|

|

Consideration for 60% shareholding |

|

250 |

|

Fair value of NCI@DOA |

|

150 |

|

FV of S's identifiable net asset |

|

|

|

share capital |

230 |

|

|

retained earning |

115 |

|

|

OCE |

10 |

|

|

FV adjust |

15 |

(370) |

|

|

|

30 |

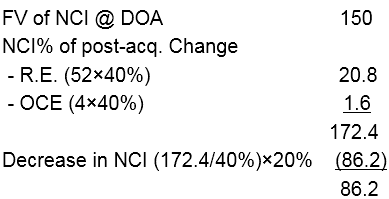

W12 N.C.I.

王老師

2021-09-09 13:08:02 1597人瀏覽

172.4是第二次購買前全部的nci,,此時的nci 它對應的是整體的40%,,第二次購買的是整體的20%,,所以需要先求整體172.4/40%,,再整體的基礎(chǔ)上乘以20%。

每個努力學習的小天使都會有收獲的,,加油,!相關(guān)答疑

-

2025-06-26

-

2025-06-14

-

2022-08-30

-

2022-07-10

-

2022-07-05

您可能感興趣的ACCA試題

- 單選題 某投資者一年前以每股40美元的價格購得股票,,每年的股息為1.50美元,。目前該股的價格為45美元,持有該股票一年的收益率是多少( ),。

- 單選題 投資者已經(jīng)收集了以下四種股票的信息: 股票 β 平均收益(%) 回報的標準差(%) W 1.0 9.5 13.2 X 1.2 14.0 20.0 Y 0.9 8.4 14.5 Z 0.8 6.0 12.0 風險最低的股票是( )。

- 單選題 公司賣出了一個看跌期權(quán),,行權(quán)價格為$56,同時購買了一個行權(quán)價格為$44的看漲期權(quán),;購買期權(quán)時股票的價格為$44,;看漲期權(quán)費為$5,看跌期權(quán)費為$4,目前的價格上漲了$7,,那么ABC公司因為看漲期權(quán)取得或是損失的金額為多少( ),。

津公網(wǎng)安備12010202000755號

津公網(wǎng)安備12010202000755號