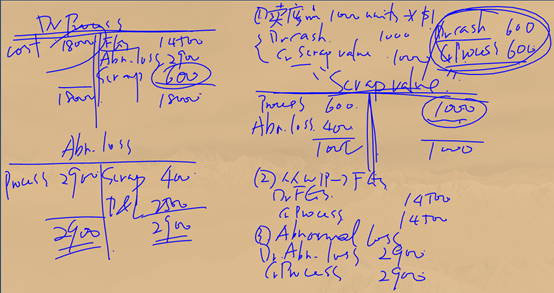

計(jì)算單位成本時(shí)如何處理報(bào)廢部分,?

這里為什么是減600,而不是減1000,,不是所有損失的產(chǎn)品都可以賣1塊錢嗎

問(wèn)題來(lái)源:

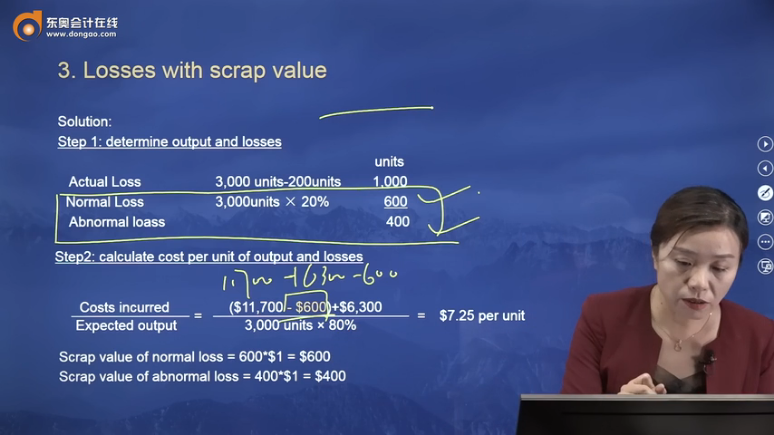

3. Losses with scrap value

Scrap is “Discarded material having some value”.

The scrap value of normal loss is usually deducted from the cost of materials.

The scrap value of abnormal loss (or abnormal gain) is usually set off against its cost, in an abnormal loss (abnormal gain) account.

Example: 3,000 units of material are input to a process. Process costs are as follows:

Material: $11,700

Conversion costs: $6,300

Output is 2,000 units. Normal loss is 20% of input.

The units of loss could be sold for $1 each.

Required: prepare a process account and the appropriate abnormal loss/gain account.

Solution:

Step 1: determine output and losses

|

|

|

units |

|

Actual Loss |

3,000 units-2000units |

1,000 |

|

Normal Loss |

3,000units × 20% |

600 |

|

Abnormal loss |

|

400 |

Step2: calculate cost per unit of output and losses

|

Costs incurred |

= |

($11,700 - $600)+$6,300 |

= |

$7.25 per unit |

|

Expected output |

3,000 units × 80% |

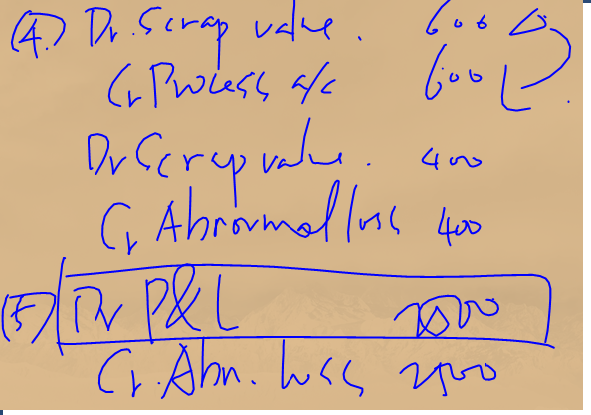

Scrap value of normal loss = 600*$1 = $600

Scrap value of abnormal loss = 400*$1 = $400

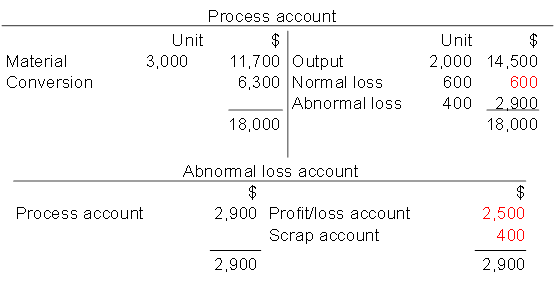

Step3: calculate total cost of output and losses

|

|

$ |

|

|

Cost of output |

2,000 units × $7.25 |

14,500 |

|

Normal loss |

600 units ×$1 |

600 |

|

Abnormal loss |

400 units × $7.25 |

2,900 |

|

Total cost |

|

18,000 |

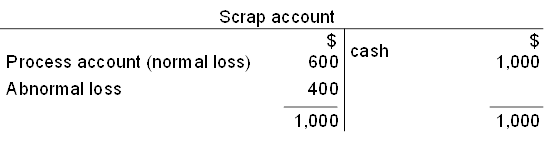

Step4: complete accounts(1)

Step4: complete accounts(2)

瞿老師

2021-10-31 14:06:44 1498人瀏覽

根據(jù)老師之前所講,報(bào)廢掉的部分分為 normal loss和abnormal loss,。

其殘值的處理方法分別為:

normal loss將從成本中抵減掉,;

abnormal loss將沖減當(dāng)期的費(fèi)用,。

由此可知這道題這里的成本只扣減normal loss的600.

詳細(xì)請(qǐng)看本節(jié)0:00-3:00的內(nèi)容。

每個(gè)努力學(xué)習(xí)的小天使都會(huì)有收獲的,,加油,!相關(guān)答疑

-

2023-11-20

-

2023-11-20

-

2023-11-20

-

2021-10-31

-

2021-10-31

您可能感興趣的ACCA試題

- 單選題 公司賣出了一個(gè)看跌期權(quán),,行權(quán)價(jià)格為$56,,同時(shí)購(gòu)買了一個(gè)行權(quán)價(jià)格為$44的看漲期權(quán),;購(gòu)買期權(quán)時(shí)股票的價(jià)格為$44,;看漲期權(quán)費(fèi)為$5,看跌期權(quán)費(fèi)為$4,目前的價(jià)格上漲了$7,,那么ABC公司因?yàn)榭礉q期權(quán)取得或是損失的金額為多少( )。

- 單選題 在理性的市場(chǎng)情況下,,下列哪個(gè)投資有可能獲得最低的回報(bào)率( )。

- 單選題 Rolling Stone公司正在考慮通過(guò)以下方式來(lái)促進(jìn)現(xiàn)金流量的增加: 鎖箱系統(tǒng):公司將在銀行設(shè)立170個(gè)賬戶,每個(gè)賬戶每月的費(fèi)用為$25,;每個(gè)月帶來(lái)利息的收入$5 240。 匯票:匯票支付每個(gè)月會(huì)發(fā)生4 000筆,,每筆花費(fèi)$2;采用匯票支付每月會(huì)節(jié)省$6 500。 銀行浮差:銀行浮差每月被用于支票支付的金額為$1 000 000,;銀行將會(huì)收取2%的服務(wù)費(fèi);但是公司將會(huì)因?yàn)楦〔钯嵢?22

津公網(wǎng)安備12010202000755號(hào)

津公網(wǎng)安備12010202000755號(hào)