問題來源:

140. A manufacturing company operates a standard absorption costing system. Last month 25,000 production hours were budgeted and the budgeted fixed production overhead cost was $125,000.

Last month the actual hours worked were 24,000 and the standard hours for actual production were 27,000.

What was the fixed production overhead capacity variance for last month?

A. $5,000 Adverse

B. $5,000 Favourable

C. $10,000 Adverse

D. $10,000 Favourable

Correct answer: A

李老師

2023-10-24 10:30:43 957人瀏覽

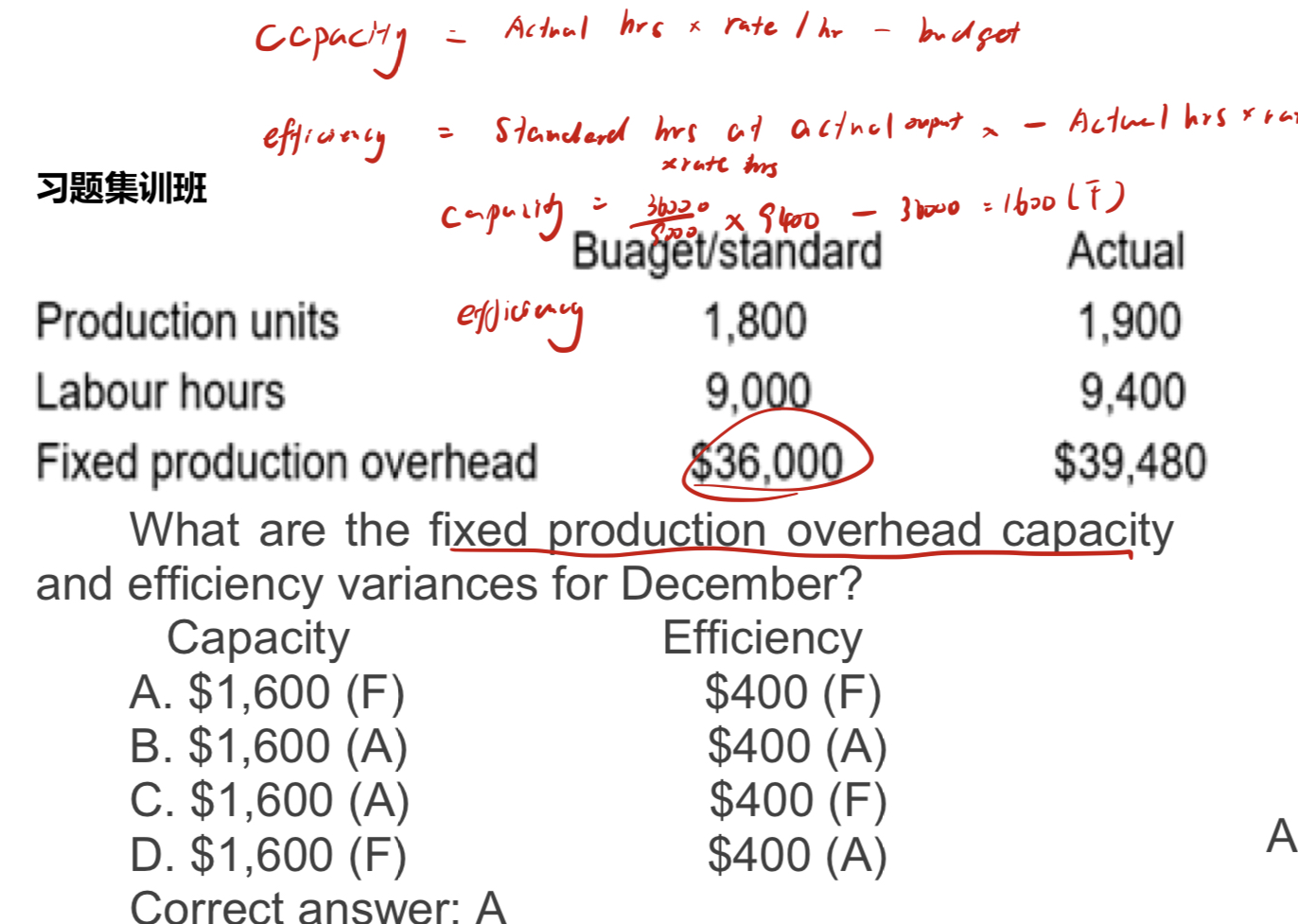

fixed production overhead volume efficiency variance

= Actual hours at standard rate/hr - Standard hrs for actual output at standard rate/hr

= 9400hours*($36000/9000) - 1900*(9000/1800)*($36000/9000) = -400

被減數(shù)是用實際工時9400乘以標準的每小時費用率($36000/9000)

每個努力學(xué)習(xí)的小天使都會有收獲的,,加油!相關(guān)答疑

-

2023-11-20

-

2023-11-20

-

2023-11-14

-

2023-11-14

-

2023-11-14

津公網(wǎng)安備12010202000755號

津公網(wǎng)安備12010202000755號