cost of capital結(jié)果評述

老師您好,

(1)請問下方截圖三段話中的最后一段怎么翻譯,?

(2)Neo老師說這道題里:business risk增加,,Vd減少,,Kd減少,;最終得出的結(jié)論是(business risk增加+Vd減少)的效用大于Kd減少的效用,,所以WACC增加,。這里的邏輯是怎么回事呢,?

(3)這張截圖是第四講Neo老師將這個(gè)知識點(diǎn)時(shí)的PPT,為什么和題里的結(jié)論不一樣

問題來源:

Sell a part of own business: 201212Q1(a)

Coeden Co is a listed company operating in the hospitality and leisure industry. Coeden Co’s board of directors met recently to discuss a new strategy for the business. The proposal put forward was to sell all the hotel properties that Coeden Co owns and rent them back on a long-term rental agreement. Coeden Co would then focus solely on the provision of hotel services at these properties under its popular brand name. The proposal stated that the funds raised from the sale of the hotel properties would be used to pay off 70% of the outstanding non-current liabilities and the remaining funds would be retained for future investments.

The board of directors are of the opinion that reducing the level of debt in Coeden Co will reduce the company’s risk and therefore its cost of capital. If the proposal is undertaken and Coeden Co focuses exclusively on the provision of hotel services, it can be assumed that the current market value of equity will remain unchanged after implementing the proposal.

Coeden Co Financial Information Extract from the most recent Statement of Financial Position

|

$000 |

|

|

Non-current assets (re-valued recently) |

42,560 |

|

Current assets |

26,840 |

|

|

|

|

Total assets |

69,400 |

|

Share capital (25c per share par value) |

3,250 |

|

Reserves |

21,780 |

|

Non-current liabilities (5.2% redeemable bonds) |

42,000 |

|

Current liabilities |

2,370 |

|

|

|

|

Total capital and liabilities |

69,400 |

Coeden Co’s latest free cash flow to equity of $2,600,000 was estimated after taking into account taxation, interest and reinvestment in assets to continue with the current level of business. It can be assumed that the annual reinvestment in assets required to continue with the current level of business is equivalent to the annual amount of depreciation. Over the past few years, Coeden Co has consistently used 40% of its free cash flow to equity on new investments while distributing the remaining 60%. The market value of equity calculated on the basis of the free cash flow to equity model provides a reasonable estimate of the current market value of Coeden Co.

Sell a part of own business: 201212Q1(a)

The bonds are redeemable at par in three years and pay the coupon on an annual basis. Although the bonds are not traded, it is estimated that Coeden Co’s current debt credit rating is BBB but would improve to A+ if the non-current liabilities are reduced by 70%.

Other Information

Coeden Co’s current equity beta is 1·1 and it can be assumed that debt beta is 0. The risk free rate is estimated to be 4% and the market risk premium is estimated to be 6%. There is no beta available for companies offering just hotel services, since most companies own their own buildings. The average asset beta for property companies has been estimated at 0.4. It has been estimated that the hotel services business accounts for approximately 60% of the current value of Coeden Co and the property company business accounts for the remaining 40%.

Coeden Co’s corporation tax rate is 20%. The three-year borrowing credit spread on A+ rated bonds is 60 basis points and 90 basis points on BBB rated bonds, over the risk free rate of interest.

Required:

(a) Calculate, and comment on, Coeden Co’s cost of equity and weighted average cost of capital before and after implementing the proposal. Briefly explain any assumptions made. (20 marks)

Answer to Sell a part of own business: 201212Q1(a)

Before implementing the proposal

Cost of Equity and Debt:

Cost of equity = 4% + 1.1 × 6% = 10.6%

Cost of debt = 4% + 0.9% = 4.9%

Market value of debt (MVd):

Per $100: $5.2 × 1.049–1 + $5.2 ×1.049–2 + $105.2 ×1.049–3 = $100.82

Total value = $42,000,000 × $100.82/$100 = $42,344,400

Market value of equity (MVe):

Assumption 1: Estimate growth rate using the rb model. The assumption here is that free cash flows to equity which are retained will be invested to yield at least at the rate of return required by the company's shareholders. This is the estimate of how much the free cash flows to equity will grow by each year.

r = 10.6% and b = 0.4, therefore g is estimated at 10.6% x 0.4 = 4.24%

MVe = 2,600 x 1.0424/(0.106 – 0.0424) approximately = $42,614,000

The proportion of MVe to MVd is approximately 50:50

Therefore, cost of capital:

10.6% ×0.5 + 4.9% × 0.5 × 0.8 = 7.3%

After implementing the proposal:

Coeden Co, asset beta estimate

1.1 × 0.5 / (0.5 + 0.5 × 0.8) = 0.61

Asset beta, hotel services only

Assumption 2: Assume that Coeden Co’s asset beta is a weighted average of the property companies' average beta and hotel services beta.

Asset beta of hotel services only:

0.61 = Asset beta (hotel services) × 60% + 0.4 × 40%

Asset beta (hotel services only) approximately = 0.75

Coeden Co, hotel services only, estimate of equity beta:

MVe = $42,614,000 (Based on the assumption stated in the question)

MVd = Per $100: $5.2 × 1.046–1 + $5.2 × 1.046–2 + $105.2 × 1.046–3 = $101.65

Total value = $12,600,000 × $101.65/$100 = $12,807,900 say $12,808,000

0.75 = equity beta × 42,614/(42,614 + 12,808 x 0.8)

0.75 = equity beta × 0.806

Equity beta = 0.93

Coeden Co, hotel services only, weighted average cost of capital

Cost of equity = 4% + 0.93 × 6% = 9.6%

Cost of capital = 9.6% × 0.769 + 4.6% × 0.231 × 0.8 = 8.2%

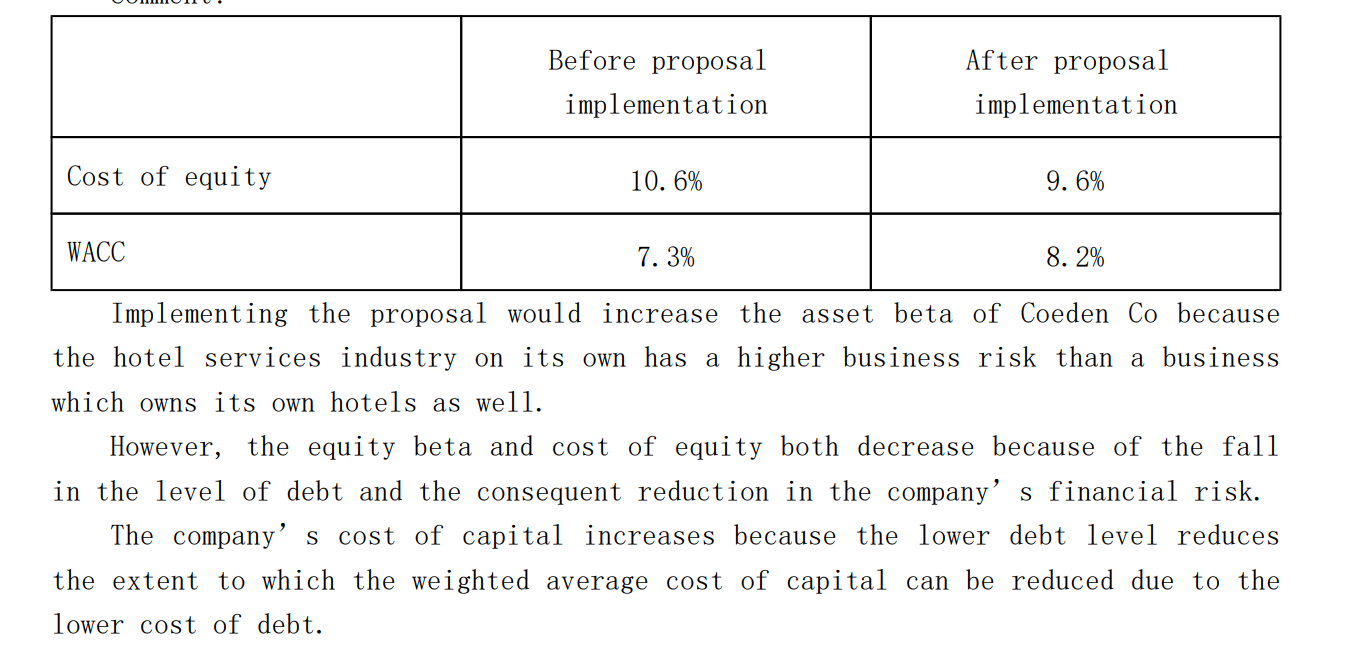

Comment:

|

Before proposal implementation |

After proposal implementation |

|

|

Cost of equity |

10.6% |

9.6% |

|

WACC |

7.3% |

8.2% |

Implementing the proposal would increase the asset beta of Coeden Co because the hotel services industry on its own has a higher business risk than a business which owns its own hotels as well.

However, the equity beta and cost of equity both decrease because of the fall in the level of debt and the consequent reduction in the company’s financial risk.

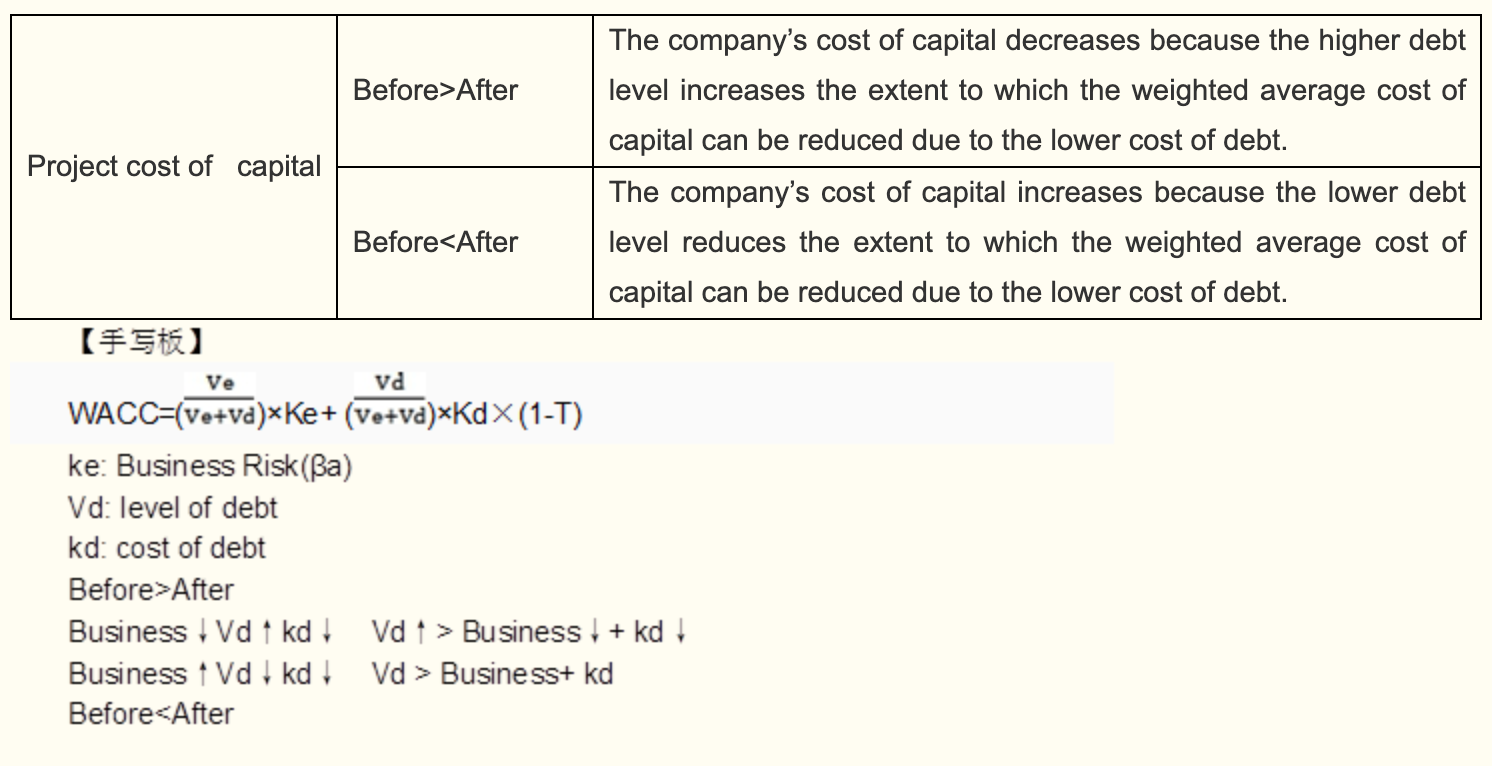

The company’s cost of capital increases because the lower debt level reduces the extent to which the weighted average cost of capital can be reduced due to the lower cost of debt.

霍老師

2021-03-09 18:01:19 824人瀏覽

哈嘍,!努力學(xué)習(xí)的小天使:

(1)公司的資本成本會升高是由于較低的債務(wù)水平對資本成本產(chǎn)生的影響大于由較低的債務(wù)成本影響的程度。

(2)這里的邏輯可以參照老師第6講中的手寫板進(jìn)行理解,。因?yàn)閃ACC=(Ve/(Ve+Vd))×Ke+ (Vd/(Ve+Vd))×Kd×(1-T)

這里的結(jié)果是WACC是上升了的(before:7.3%,,after:8.2%)。首先,,business risk(asset β)上升,,Vd和Kd是減少的,那么要是的最終WACC上升就必須是(business risk+Vd)也就是Ke對WACC產(chǎn)生的影響要大于Kd的減少,,否則WACC是不可能增加的,。

(3)老師第6講中是筆誤,在之前的答疑中給您答過,,應(yīng)該是decrease,,后期會進(jìn)行修改,這里是沒有問題的,。

每個(gè)努力學(xué)習(xí)的小天使都會有收獲的,,加油!

相關(guān)答疑

-

2023-03-02

-

2023-02-27

-

2023-02-20

-

2021-03-11

-

2021-03-11

您可能感興趣的ACCA試題

- 單選題 IMA管理會計(jì)聲明中“價(jià)值觀和道德觀:從接受到實(shí)踐”表明持續(xù)的培訓(xùn)應(yīng)包括下列所有內(nèi)容,,除了( )。

- 單選題 某投資者一年前以每股40美元的價(jià)格購得股票,,每年的股息為1.50美元。目前該股的價(jià)格為45美元,,持有該股票一年的收益率是多少( ),。

- 單選題 投資者已經(jīng)收集了以下四種股票的信息: 股票 β 平均收益(%) 回報(bào)的標(biāo)準(zhǔn)差(%) W 1.0 9.5 13.2 X 1.2 14.0 20.0 Y 0.9 8.4 14.5 Z 0.8 6.0 12.0 風(fēng)險(xiǎn)最低的股票是( ),。

津公網(wǎng)安備12010202000755號

津公網(wǎng)安備12010202000755號