RS進(jìn)入RE后能否分紅?RS如何消失,? RS進(jìn)入RE后能否給股東分紅,?RS如何消失?

問(wèn)題來(lái)源:

6. Subsequent measurement——revaluation model

后續(xù)計(jì)量要解決的問(wèn)題是,,在每一個(gè)資產(chǎn)負(fù)債表日,某項(xiàng)資產(chǎn)或負(fù)債要以什么金額最終列示在資產(chǎn)負(fù)債表上的問(wèn)題,。

Revaluation model

When a non-current asset is purchased we record them at their initial cost. However, over time these values may materially differ from their market value. The most common example is land and building.

In order to overcome this issue I.A.S. 16 allows companies to reflect the fair value in the statement of financial position. Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date ( i.e. it is an exit price) .

This policy may be adopted, and if so the following rules must be applied per the standard:

? If a company chooses to revalue an asset they must revalue all assets in that category at the same time

? Revaluations must be regular

? Subsequent depreciation must be based on the revalued amounts

? Gains from revaluations are NOT taken to the income statement as no gain has been realized. Instead, it is recognised in the statement of comprehensive income, as one of the "other comprehensive income (OCI)".

Example:

(1) A building was purchased at 1 Jan. 2000 for $500,000 with a useful life of 25 years.

(2) It was revalued to $1,200,000 at 1 Jan. 2015 and overall useful life remained unchanged.

(3) It was disposed at 1 July 2016 and sold for $1.05m.

Cost @1 Jan. 2000 500,000

A.D. @31 Dec. 2014 (300,000)

N.B.V @1 Jan. 2015 200,000

Gain on revaluation 1,000,000

Revalued amount 1,200,000

Cost @1 Jan. 2000 500,000

A.D. @31 Dec. 2014 (300,000)

N.B.V @1 Jan. 2015 200,000

Gain on revaluation 1,000,000

Cost @ 1 Jan. 2015 1,200,000

Depn. for 2015 (1.2m/10) (120,000)

N.B.V @31 Dec. 2015 1,080,000

I/S for 2015

Sales 0

Depn. Expense (120,000)

Net loss (120,000)

O.C.I.

Gain on revaluation 1,000,000

B/S as at 31 Dec. 2015

Asset

N.C.A.

PPE 1,080,000

Equity 調(diào) 不調(diào)

R.S. 900,000 1,000,000

R.E. (20,000) (120,000)

880,000 880,000

Cost @1 Jan. 2000 500,000

A.D. @31 Dec. 2014 (300,000)

N.B.V @1 Jan. 2015 200,000

Gain on revaluation 1,000,000

Revalued amount 1,200,000

N.B.V @31 Dec. 2015 1,080,000

Depn. for 6mths (60,000)

N.B.V before disposal 1,020,000

Profit on disposal 30,000

Proceed on disposal 1,050,000

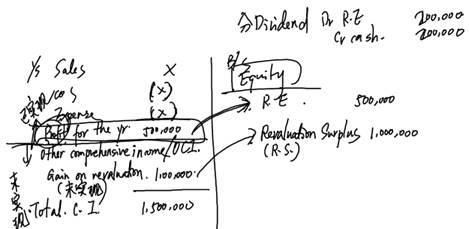

總結(jié):R.S.的實(shí)現(xiàn)途徑有兩種

(1)每年從R.S.調(diào)進(jìn)R.E.

(2)在資產(chǎn)處置時(shí),,一次性實(shí)現(xiàn)進(jìn)R.E.

以上兩種情況,都不是compulsory,,只是optional (注意處理相關(guān)的選擇題),,且固定資產(chǎn)重估價(jià)增值的部分永遠(yuǎn)不會(huì)影響損益表。

于老師

2021-10-12 14:54:59 982人瀏覽

1. RS實(shí)現(xiàn)進(jìn)RE后,,才能分dividend

2. RS 實(shí)現(xiàn)有兩種方式,Excess Depn每年調(diào)減RS,,disposal一次性實(shí)現(xiàn),,兩種方式皆調(diào)增RE,屬于權(quán)益內(nèi)變動(dòng),,不影響損益表,。不轉(zhuǎn)RE的部分一直在OCI里了。

希望可以幫助到您O(∩_∩)O~相關(guān)答疑

-

2025-06-26

-

2025-06-14

-

2024-10-27

-

2022-03-21

您可能感興趣的ACCA試題

- 單選題 某投資者一年前以每股40美元的價(jià)格購(gòu)得股票,每年的股息為1.50美元,。目前該股的價(jià)格為45美元,,持有該股票一年的收益率是多少( )。

- 單選題 投資者已經(jīng)收集了以下四種股票的信息: 股票 β 平均收益(%) 回報(bào)的標(biāo)準(zhǔn)差(%) W 1.0 9.5 13.2 X 1.2 14.0 20.0 Y 0.9 8.4 14.5 Z 0.8 6.0 12.0 風(fēng)險(xiǎn)最低的股票是( ),。

- 單選題 公司賣(mài)出了一個(gè)看跌期權(quán),行權(quán)價(jià)格為$56,,同時(shí)購(gòu)買(mǎi)了一個(gè)行權(quán)價(jià)格為$44的看漲期權(quán),;購(gòu)買(mǎi)期權(quán)時(shí)股票的價(jià)格為$44;看漲期權(quán)費(fèi)為$5,看跌期權(quán)費(fèi)為$4,,目前的價(jià)格上漲了$7,,那么ABC公司因?yàn)榭礉q期權(quán)取得或是損失的金額為多少( )。

津公網(wǎng)安備12010202000755號(hào)

津公網(wǎng)安備12010202000755號(hào)