問題來源:

4. Depreciation Accounting

Depreciation is the charge to the statement of profit or loss to reflect the consumption of an asset in a period. By applying depreciation charges, we are consistent with the ACCRUALS / MATCHING CONCEPT i.e. applying the cost of using the asset to the statement of comprehensive income for the same period.

All tangible non-current assets should be depreciated on a systematic basis per I.A.S. 16, with the exception of land.

This is because land is seen to appreciate in value.

Intangible non-current assets are amortized over their useful economic life (this is just another term for depreciation).

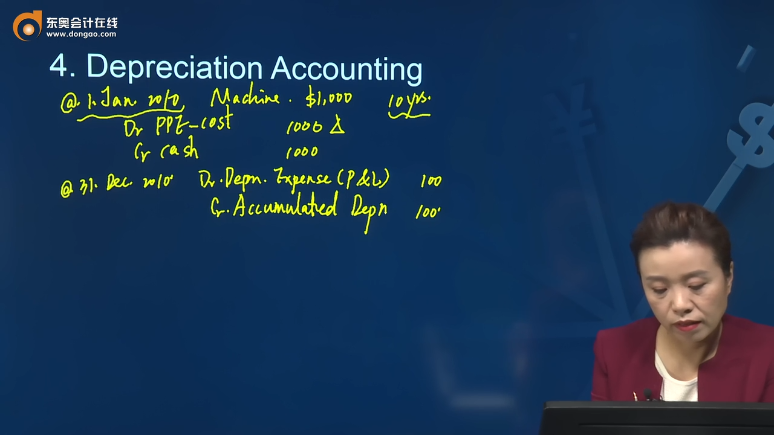

4.1 Depreciation has dual effects:

(a) depreciation is charged as an expense in the P&L account

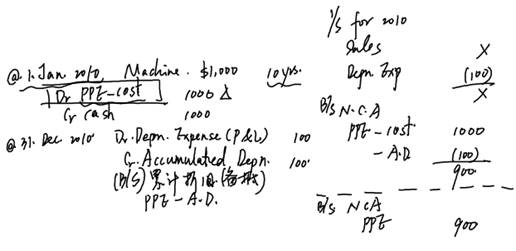

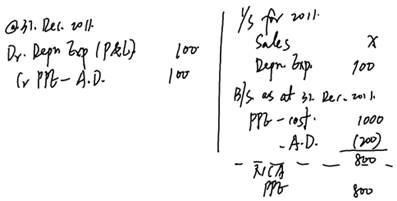

(b) The corresponding credit is accumulated in the provision for depreciation account in the balance sheet to offset against the original cost of the fixed assets.

Dr Depreciation expense xx

Cr Accumulated Depreciation xx

1.5 Residual value of an asset is the estimated amount that an entity would currently obtain from disposal of the asset, after deducting the estimated costs of disposal, if the asset were already of the age and in the condition expected at the end of its useful life.(IAS16)

1.6 Carrying amount (Net book value) is the amount at which an asset is recognized after deduction any accumulated depreciation and accumulated impairment losses.

The balance of accumulated depreciation on the SOFP is the total accumulated depreciation. This is always a credit balance brought forward in the ledger account for depreciation. The non-current asset accounts are unaffected by depreciation. In the SOFP of a business, the total balance on the "Accumulated Depreciation" account is set against the value of non-current asset account to derive the NBV of the non-current asset.

4.2 Depreciation methods

The depreciation method used shall reflect the pattern in which the asset's future economic benefits are expected to be consumed by the entity.

4.2.1 Straight line method 直線折舊法

Depreciation per annual =Original cost – estimated residual value

Estimated useful Life

4.2.2 Reducing balance method 余額遞減法/加速折舊

This method of depreciation is generally used for assets which tend to lose more value in the initial years and require greater maintenance in the later years. A good example would be a brand new motor vehicle. Motor vehicles tend to depreciate rapidly in the earlier years and require very little maintenance.

Depreciation per annual = Depreciation rate% × opening NBV

Example:A machine was bought on 1 Jan. 2010 for $5,000, with useful life 6 years. It is depreciated on reducing balance method with reducing rate 20%.

Year Opening NBV×20% Depn. Exp. A.D. NBV

1 5000*20% 1,000 1,000 4,000

2 4,000*20% 800 1,800 3,200

3 3,200*20% 640 2,440 2,560

于老師

2021-10-07 19:41:35 936人瀏覽

備抵科目(Contra account)是資產(chǎn)的備抵科目,,貸記表增加,,余額在貸方,用來抵減資產(chǎn)在B/S上的列示金額,。

PPE原值與累計折舊在資產(chǎn)負債表上分別列示,,原值即原值不能夠沖減,有備抵科目的資產(chǎn),,都是以歷史成本屬性計量。PPE-cost科目余額是資產(chǎn)的歷史成本(原值),,不能隨意變動,。所以用備抵科目記錄減值,攤銷,,折舊等等,,如壞賬疑賬計提壞賬準備的'Allowance',無形資產(chǎn)的累計攤銷皆使用備抵科目,。

希望可以幫助到您O(∩_∩)O~相關答疑

-

2025-06-26

-

2025-06-14

-

2024-10-27

-

2022-03-21

您可能感興趣的ACCA試題

津公網(wǎng)安備12010202000755號

津公網(wǎng)安備12010202000755號